2016 forecast

The VisitBritain forecast for the volume and value of inbound tourism is issued in December each year.

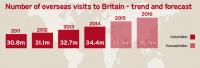

Our forecast for visits for the full year 2015 is 35.4m visits, an increase of 2.8% on 2014. Our forecast for spending by visitors in 2015 is £22.0bn, a 0.7% increase on 2014.

Our forecast for 2016 is for 36.7 million visits, an increase of 3.8% on 2015; and £22.9bn in visitor spending, an increase of 4.2% on 2015.

We have identified a number of risks as briefly detailed below and will continue to monitor our forecasts.

A number of economic assumptions underpin these forecasts. The Eurozone economy is expected to continue to grow at a moderate pace in 2016, perhaps fractionally stronger overall than in 2015. The US economy is expected to grow at a similar rate as it did in 2015.

The wider global economic outlook remains uncertain. In 2015, the Chinese economy slowed, the Eurozone saw a period of deflation, the oil price continued to fall and some major emerging markets experienced recession. In 2016, a number of emerging markets are expected to continue to see weak growth although China and India are assumed to be among the world’s fastest-growing economies.

Exchange rates have been volatile in recent years. These not only colour value perceptions of destinations but affect visitors’ budgets. In 2015, the pound rose in value against many major currencies, one reason we expect spending to have grown at a slower rate than visit numbers. For the 2016 forecast, the Euro is assumed to be broadly stable against the Pound in 2016 while the US dollar is expected to appreciate slightly.

Interest rate policy decisions affect exchange rates as well as the broader macroeconomic picture. We expect the Bank of England to raise its base rate during the second half of 2016.

The global price of oil fell in late 2015. This is an important indicator as it not only affects the cost of transportation but real disposable incomes for consumers around the world. At the time the forecast was produced the oil price was above $45/barrel; if the oil price remains much below $40 throughout 2016 then this would boost disposable incomes for visitors from many, though not all, markets.

2016 will not see a major international sporting event held in Britain (aside from those held annually), unlike in many recent years. However, it will be a big year for the arts with a number of Britain’s musical and literary legends celebrating significant anniversaries and milestones in 2016, including the 400th anniversary of Shakespeare's death and the 100th anniversary of Roald Dahl’s birth. Adding to a year of art and culture, 2016 will also see the opening of new galleries, performances and productions: the National Museums of Scotland will open ten new galleries; the new Tate Modern will open in June; the highly anticipated play ‘Harry Potter and the Cursed Child’ debuts in July.

It is assumed that there will be no unforeseen major events that significantly disrupt travel to Britain, e.g. related to geopolitics, health scares or natural disasters. Events in late 2015 underline that geopolitical / security developments remain a risk.

There are both upside and downside risks for 2016. Recent currency volatility and the uncertainties in forecasting the value of Sterling against major currencies, as well as volatility in the inflation rate in recent years, means that the forecast range for spending is greater than that for visits.